Alternative Lenders: Where They Thrive and Where They Are Weak

Report Summary

Alternative Lenders: Where They Thrive and Where They Are Weak

Alternative lenders could become stronger by tapping into the human networks that influence credit-seeking SMBs.

Boston, February 8, 2018 – Alternative lenders are commonly feared due to their reputations for superior customer service, fast turnaround times, and rapid acquisitions of market share. With folklore and fear driving their perceptions of these new competitors, banks have responded with various combinations of denial, collaboration, competition, emulation, and coopetition. But if folklore and fear were to be replaced by data and facts, what would an accurate perception of the alternative lenders be? And what, therefore, would be an appropriate competitive response for banks?

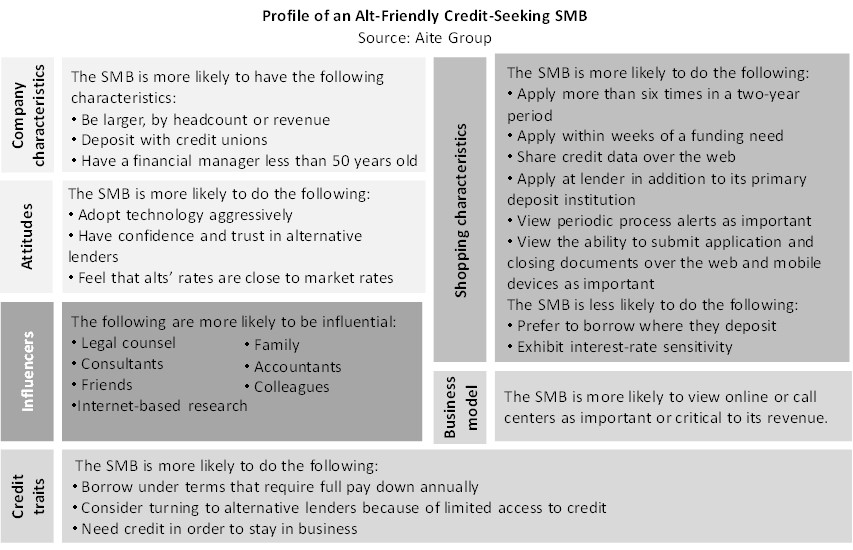

It is in the context of the arrival of the alternative lenders and banks’ range of potential reactions to them that Aite Group has undertaken an analysis of alternative lenders to determine where they thrive and where they are weak. In August 2016, Aite Group fielded an online survey of 601 U.S. small and midsize businesses (with annual revenue of US$100,000 to US$20 million). This Impact Note focuses on the respondents that have applied for a loan in the last two years and fit into the alt-averse credit-seeking SMBs and alt-friendly credit-seeking SMBs categories.

This 23-page Impact Note contains two figures and 25 tables. Clients of Aite Group’s Wholesale Banking & Payments service can download this report, the corresponding charts, and the Executive Impact Deck.

![]()

This report mentions CRIF, Cloud Lending Solutions, Finastra, FIS, Fiserv, Genpact, IBM, Jack Henry, LexisNexis Risk Solutions, Linedata, Moody's Analytics, nCino, Nucleus Software, Oracle, Polaris, Provenir, Wipro, and Wolters Kluwer Financial Services.