Leveraging the Online Channel to Deepen Small-Business Relationships

Report Summary

Leveraging the Online Channel to Deepen Small-Business Relationships

Banks trying to appeal to small businesses cannot ignore the online channel. Of U.S. small businesses, 65% will actively bank online by the end of 2008.

Boston, MA, November 3, 2008 – A new report from Aite Group, LLC examines the key issues currently challenging the online small-business banking strategies of large U.S. banks, and provides insight into their plans for overcoming them. It also analyzes key online product/function adoption rates, current capabilities, planned offering enhancements, and areas of bank focus in the next 24 months.

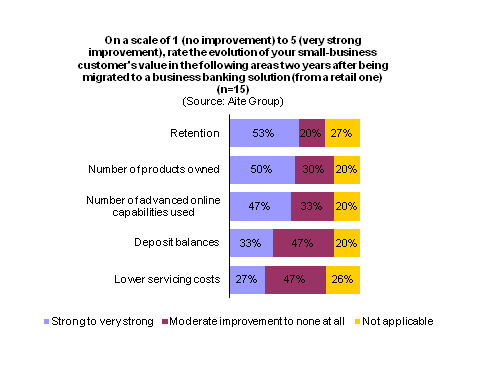

Forty-one percent of U.S. small businesses prefer to interact with their banks via the online channel than through any other channel. Additionally, according to an Aite Group survey of 16 of the 50 largest U.S. banks conducted from July to September 2008, 81% of large banks rate their small-business customer's level of trust in online banking as "high to very high," compared to the 33% that felt this way 24 months ago. These are numbers that banks cannot afford to ignore, and the online channel is one which banks should strive to fully leverage. Most banks, however, currently limit small-business options by serving them on consumer solutions, and do not yet have fully developed online offerings for these customers. Aite Group's research reveals the potential for deeper relationships and greater small-business customer retention as a result of migration to a business banking solution. Fifty-three percent of banks surveyed are seeing much greater customer retention as a result of migrating their small-business customers from a retail banking platform over to a business banking platform, while others are seeing a greater number of both products (50%) and advanced online capabilities (47%) used as a result of migration, at 50% and 47%, respectively.

"Because 70% of small businesses consider a bank's online capabilities when selecting their primary institution, it is essential that banks enhance their online offerings and add crucial capabilities to save small businesses time and add convenience," says Christine Barry, research director with Aite Group and author of this report. "Banks are waking up to the need to provide enhanced online services to small businesses. Over the next 24 months, large banks will be adding expedited bill payment capabilities (38%), electronic invoice presentment and payments (31%) and cash concentration (31%) to their online small-business banking offerings. Personal financial management and cash flow tools for more efficient management of cash are also receiving a great deal of attention and consideration."

This 23-page Impact Note contains 22 figures. Clients of Aite Group's Wholesale Banking service can download the report.