Reassessing Capital Risk in Commercial Real Estate Portfolios: Stress for All?

Report Summary

Reassessing Capital Risk in Commercial Real Estate Portfolios: Stress for All?

Capital planning and risk assessment is now becoming mandatory for smaller institutions, which are often ill-prepared to meet the requirements.

Boston, June 12, 2012 – A new report from Aite Group looks at the state of commercial credit offerings at U.S. banks and credit unions and discusses new rules and guidance that will affect commercial lending. It examines bank and credit union responses to regulatory oversight and advises on solutions and tools that are available to help institutions navigate an essentially new environment.

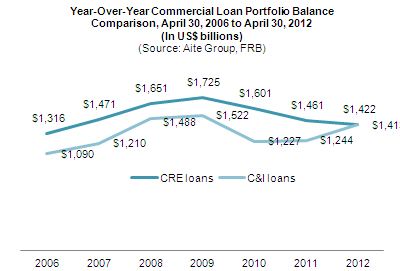

The credit industry as a whole has been fixated on consumers for some time now, but regulators have recently begun to focus their attention on commercial credit. Regulators are zeroing in on the real estate portfolios of banks across all parts of the spectrum, from super-regional banks to large and small community banks to credit unions. All of these institutions are being met, often during safety and soundness exams, with unwelcome mandates to “know your portfolio” in excruciating detail.

“For all but the largest of institutions, the requirement to begin a monthly assessment of capital risk in commercial real estate (CRE) portfolios has come as something of a surprise,” says Christine Pratt, senior analyst with Aite Group and author of this report. “As of Q1 2012, examiners began to ‘suggest’ that banks with assets well below the US$100 billion range acquire the tools and analytics necessary to assess capital risk in their CRE portfolios as often as monthly."

This 22-page Impact Note contains five figures and three tables. Clients of Aite Group’s Wholesale Banking service can download the report.