Wirehouses and Registered Investment Advisors: So Alike Yet So Different

Report Summary

Wirehouses and Registered Investment Advisors: So Alike Yet So Different

Despite their traditional differences, wirehouse and RIA firms increasingly compete for advisors and client assets.

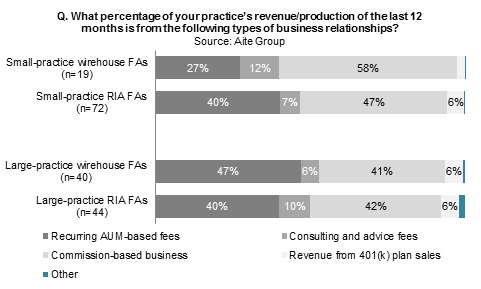

Boston, March 12, 2013 – A new report from Aite Group reveals and compares a broad range of qualities across wirehouse- and RIA-affiliated advisors. Based on a March 2012 Aite Group survey of 534 financial advisors, the report segments advisors by asset size and channel; it also highlights important differences in advisor attributes, investment products used, asset management styles, revenue production, income, practice structure, and time allocation.

The 2008 financial crisis greatly impacted the U.S. wealth management industry, and advisors at wirehouse and RIA firms are feeling the change. While wirehouse and RIA segments at first glance differ significantly, the financial crisis turned the tables on these players. The fragmented RIA segment has grown steadily in recent years, thanks to a flow of breakaway brokers from wirehouse firms, but the once-mighty wirehouses struggled to make it through the crisis intact. Advisor movement, coupled with blurring business models across these historically different channels, has resulted in more direct competition between them, with the scrappy RIA channel proving a tough competitor.

“Striking similarities exist between wirehouse- and RIA-affiliated advisors,” says Bill Butterfield, analyst with Aite Group and co-author of this report. “But across a host of similarities, a few key distinctions will mean the difference between retaining advisors and assets and losing them.”

This 37-page Impact Report contains 23 figures and two tables. Clients of Aite Group’s Wealth Management service can download the report.