U.S. Mobile Payments: The Time Has Come

Report Summary

U.S. Mobile Payments: The Time Has Come

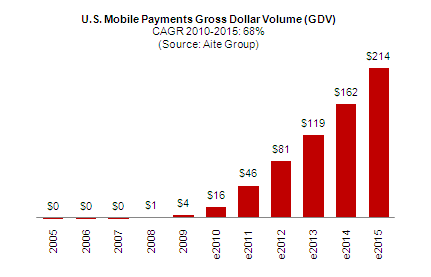

Aite Group forecasts that U.S. mobile bill payments will reach US$214 billion in gross dollar volume in 2015, up from US$16 billion in 2010.

Boston, November 17, 2010 – A new report from Aite Group provides a roadmap to mobile payments in the United States, defining and segmenting the mobile payments universe and examining the competitive and market trends shaping the space. Based on more than 60 Aite Group interviews with industry stakeholders in September and October 2010, the report sizes and projects the growth of mobile payments in the United States over the next few years, and provides snapshots of key stakeholders operating in the space.

Long seen as a laggard in mobile payments, the United States is far more ahead of the curve than perceived. Over the past 12 to 18 months, the United States has begun to move closer to a tipping point that will lead to the popularization of mobile payments. Factors laying the foundation for mobile payments to grow in coming years include rapid consumer adoption of smartphones, carriers’ and handset manufacturers’ adoption of NFC chips, consumers’ continued embrace of m-commerce, and a nationwide increase in mobile banking adoption.

Practically no segment will be left behind; in fact, each one of the multiple categories of mobile payments defined in the report will experience double-digit growth. Mobile payments will account for US$214 billion in gross dollar volume by 2015, up from US$16 billion in 2010--a 68% compound annual growth rate (CAGR) between 2010 and 2015.

“Firms missing the signs that the market is now rapidly shifting will be at a serious disadvantage in the next few years,” says Gwenn Bézard, research director with Aite Group and author of this report. “Many organizations within the industry remain unaware that mobile payments are in a period of rapid transformation. Those that have any desire to play a role in this market must wake up now.”

The report references the following mobile payments firms in some capacity: Allstate, Amazon, American Express, Apple, AT&T, Bango, Bank of America, Barclays, Bill2Mobile, BlackBerry, Bling Nation, BOKU, Brink’s, C-Sam, Cashedge, Cellfire, Chase, Chase Paymentech, Cimbal, ClairMail, coupons.com, Coupons Sherpa, Visa’s Cybersource, Cimbal, Device Fidelity, Diebold, Discover, Eagle Eye Solutions, eBay, Euronet, Facebook, First Data, FIS, Fiserv, Foursquare, Gemalto, Global Payments, Google, Gowalla, Green Dot, Groupon, Harland Financial Services, Heartland Payment Systems, Hipcricket, iLoop Mobile, Inside Contactless, Intuit, Jack Henry/iPay Technologies, Kubra, MasterCard, mFoundry, Mobile Coupons, Mocapay, MoneyGram, Monitise Group, mopay, MyWebGrocer, NCR, NetSpend, Nokia, Oberthur Technologies, Obopay, OfferIQ, Online Resources, PayPal, Plastyc, Pyxis Mobile, Research-in-Motion (RIM), Roam Data (Ingenico), Roamware, Rocketbuxx, SK C&C USA, Square, Starbucks, Sybase, T-Mobile, Tetherball, 3i Infotech, Tier Technologies, TransferTo, TSYS, Twitter, U.S. Bank, VeriFone, Verizon, Vesta, Visa, ViVOtech, Waspit, Way Systems, Western Union, Wincor Nixdorf, WirelessLoyalty, Xipwire, Yelp, and Zong.

This 65-page Impact Report contains 27 figures and 11 tables. Clients of Aite Group's Retail Banking service can download the report.