Merchant Acquiring and the Durbin Amendment

Report Summary

Merchant Acquiring and the Durbin Amendment

The merchant acquiring industry is expected to benefit from increased margins due to the Durbin Amendment, but only for a short time.

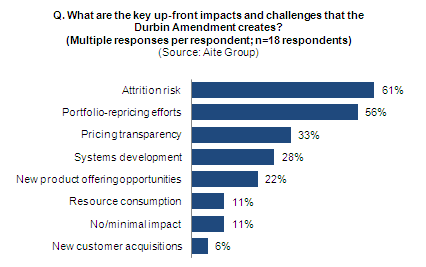

Boston, September 15, 2011 – A new report from Aite Group provides insight into the impact the Durbin Amendment will have on merchant acquiring. Based on July and August 2011 Aite Group interviews with 18 executives at acquiring organizations, the report assesses the expected impact of the Durbin Amendment on acquiring, risk, and risk mitigation.

On June 29, 2011, the Federal Reserve Board issued final regulations relating to debit interchange and transaction routing per section 1075 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, also known as the “Durbin Amendment.” These new regulations create a debit and prepaid interchange cap, mandate the types of financial institutions to which the cap will apply, and require that prepaid cards use at least two unaffiliated networks for transaction routing. While some industry executives believe the impact of the Durbin Amendment will be limited, most see potential near-term benefits from enhanced margins. Most also agree, however, that these benefits will be short-lived. As competing acquirers reduce fees, merchant attrition risk will become a major issue, forcing the rest of the industry to follow suit.

“Price compression in merchant acquiring has meant that opportunities to increase margins have been somewhat rare,” says Rick Oglesby, senior analyst with Aite Group and co-author of this report. “The Durbin Amendment provides one of these rare opportunities, and merchant acquirers are preparing to take advantage of it while it lasts. While many see the incremental margin as a creator of incremental attrition risk, most are prepared to take that risk, and are enhancing retention strategies in preparation.”

This 17-page Impact Note contains 11 figures. Clients of Aite Group's Retail Banking service can download the report.