IT Spending on Retail Credit Default Solutions: If You Build It, Will They Come?

Report Summary

IT Spending on Retail Credit Default Solutions: If You Build It, Will They Come?

Portfolio metrics and new regulations are driving lenders to invest in retail credit default solutions.

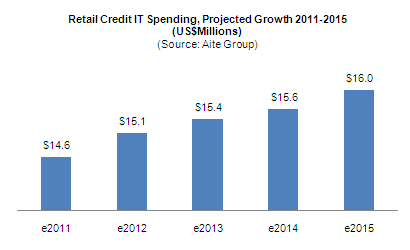

Boston, March 14, 2011 – A new report from Aite Group provides an overview of the U.S. retail credit business environment, focusing on changes in default operations. The report explores portfolio metrics, emerging regulatory challenges, and the impact of consolidation and convergence on technology choices. It also projects U.S. lending institutions’ IT spending on default systems and solutions through 2015.

Managing high levels of retail credit risk, delinquencies, and losses is unfamiliar territory for many U.S. lenders. Faced with increasingly high loan default rates, steeply declining loan balances and earnings, and large volumes of loans to service, lending executives are focusing immediate and significant attention on software solutions that improve processing efficiency, and analytics that advance the understanding and management of risk. Many lenders plan to invest in innovative default management solutions in the next two to five years, with much of this investment directed at third-party providers.

“For lenders, managing defaults has never been more challenging,” says Christine Pratt, senior analyst with Aite Group and author of this report. “In the coming years, driven by the rapid rise in distressed loans and an onslaught of regulatory initiatives, IT spending among lenders is expected to be brisk and heavily focused in the areas of software and analytics to support default processes.”

This 19-page Impact Note contains five figures and four tables. Clients of Aite Group's Retail Banking or Wholesale Banking service can download the report.