European Dark Trading: Who’s Playing in Your Pool?

Report Summary

European Dark Trading: Who’s Playing in Your Pool?

Europe’s dark trading venues provide traders with liquidity, but multiple venues serve different purposes.

London, 13 December 2010 – A new report from Aite Group discusses how European dark venues differ from one another, and how these differences demand an understanding from traders in the European market. Based on Aite Group conversations with execution venues, broker/dealers, and buy-side traders, the report also sheds light on how specific factors – such as post-trade reporting irregularities – impact market participants’ opinions of dark pools. It also discusses the misconceptions about OTC trading and dark trading, held by many market participants, regulators, and European Parliament.

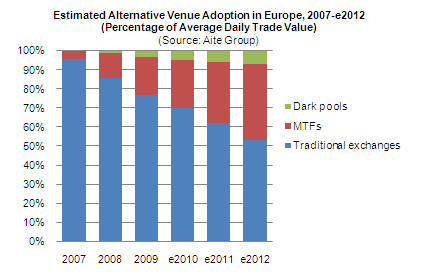

Along with other factors, the proliferation of electronic trading has led to decreased trade sizes and increased difficulty in liquidity sourcing. As a result, traders have turned to alternative execution venues, including dark pools, to execute trades. Defined as execution venues that do not provide displayed quotes, dark pools’ core value is their ability to provide access to liquidity while minimizing market impact. The non-displayed market lacks homogeneity, however, mirroring the variety of different needs of market participants in the current environment. As such, market participants must understand their own needs and the capabilities of multiple dark venue options.

“Ultimately, it is up to market participants to understand dark venues based upon the stocks that are being traded in them and the types of market participants with which they are interacting,” says Simmy Grewal, analyst with Aite Group and author of this report. “Once participants understand these things, they can interact with the market in accordance with their own, unique trading style. Post-trade analysis of executions across venues should help traders understand which venues may complement their trading style and which might hinder it.”

The report provides trading information on dark venues operating in Europe, including BATS Europe Dark Pool, Chi-X’s Chi-Delta, NADAQ OMX’s Nordiq@Mid, NYSE Euronext’s SmartPool, Turquoise’s TQ Dark Midpoint Order Book, Citi’s CitiMatch, Credit Suisse’s Crossfinder, Knight Capital’s Knight Link, Barclays Capital’s LX (Liquidity Cross), Morgan Stanley’s MS Pool, Nomura’s Nomura SI and NX MTF, UBS’s UBS MTF and UBS Pin, ICAP’s Blockcross, Instinet’s Blockmatch, ITG’s POSIT, Liquidnet, and Pipeline Financial Group’s Pipeline Europe - Block Board.

This 28-page Impact Note contains 10 figures and 11 tables. Clients of Institutional Securities & Investments service can download the report.