Demystifying Payments Hubs

Report Summary

Demystifying Payments Hubs

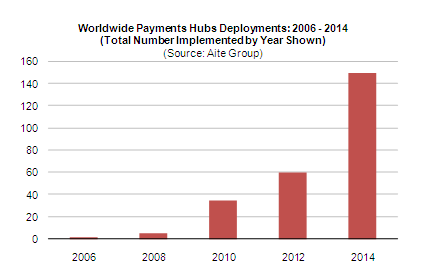

Though bank adoption of payments hubs has been slow, Aite Group expects the number of banks with payments hubs will rise by 62% CAGR through 2014.

Boston, MA, December 22, 2008 – A new report from Aite Group, LLC examines global banks' use of payments hubs. The report presents three examples of banks that have implemented payments hubs, and the factors that contributed to their choice of payments hub implementation. These examples demonstrate the variety of payments hub implementations available, and highlight individual bank business strategies supported by the payments hubs. This note discusses the diversity of technology vendors developing payments hubs, and their respective approaches. Finally, it projects the adoption of payments hubs by banks globally and identifies payments hub success criteria for banks and technology vendors.

Most banks' operations, product management, customer servicing and IT departments are currently structured in silos to support individual payments types - check or paper draft, ACH, wire transfer, card (credit, debit, prepaid, corporate, fleet, purchasing, etc.), automated teller machine (ATM) and kiosks. Each of these payments types typically has its own fraud prevention and regulatory compliance components, resulting in redundant systems, lack of transparency across payments systems, and less than optimal customer service.

The deployment of a payments hub can integrate a bank's disparate payments processing systems. This can be accomplished by replacing an existing system or by adding a middleware layer to handle common functions and interface with back-end systems. In creating a payments hub, the bank is able to provide transparency into the status of payments processing, thus facilitating management decision-making and enhancing the bank/client relationship.

"In today's economic environment, in which banks' priorities are to cut costs while generating new revenue sources and strengthening risk management, payments hubs serve as a way to accomplish those goals," says Nancy Atkinson, senior analyst with Aite Group and author of this report. "While an implementation of a payments hub can take many years, the timeframe should not stop banks from establishing a team to assess the optimal approach for their institution to take. With a multiyear migration plan in place, banks can begin to see positive incremental results right away."

Vendors mentioned in the report include: ACI Worldwide, Bottomline Technologies, CheckFree (a Fiserv Company), Fundtech, S1, SunGard, Fidelity National Information Services, Metavante, Misys, Clear2Pay, Dovetail Systems, TietoEnator, Sterling Commerce, IBM, i-flex (an Oracle company), Infosys, TCS, Unisys and SWIFT.

This 25-page Impact Note contains one figure and four tables. Clients of Aite Group's Wholesale Banking service can download the report.