The Borrowing Habits of Alternative Financial Services Customers

Report Summary

The Borrowing Habits of Alternative Financial Services Customers

While stigma and misunderstanding surround the use of alternative financial services in the United States, users of these services don’t fit preconceived molds.

Boston, June 2, 2011 – A new report from Aite Group examines the use of alternative financial services like prepaid cards, payday loans, check-cashing services, pawn shops, loan sharks, and even family and friends, as a source of funds for customers of alternative financial services. Based on a Q1 2011 Aite Group survey of 500 U.S. consumers, the report evaluates how consumer use of these services changed between 2009 and 2010.

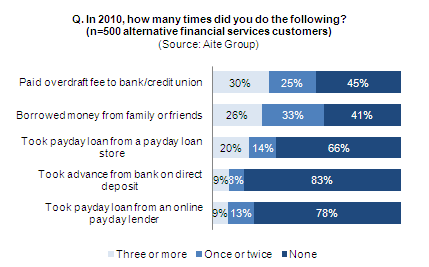

There is a good deal of stigma and misunderstanding surrounding the use of alternative financial services in the United States; alternative financial services are often seen as a source of funds for those with few alternatives. In reality, most of these consumers are neither disadvantaged nor unbanked/underbanked individuals: 78% of respondents have a checking account, three-quarters have a debit card tied to that checking account, nearly half have a credit card, and roughly one in five currently have (or had at some point in 2010), a payroll card or government benefit card.

“Making assumptions about the users of alternative financial services should be avoided,” says Ron Shevlin, senior analyst with Aite Group and co-author of this report. “These services provide value to those who choose to use them. There’s strong evidence that customers of alternative financial services are not trapped in a cycle of using these services, nor are they necessarily unbanked or underbanked.”

This 33-page Impact Note contains 21 figures and five tables. Clients of Aite Group's Retail Banking services can download the report.