U.S. Consumer Bill Payment and Presentment: A Biller Survey, Part Two

Report Summary

U.S. Consumer Bill Payment and Presentment: A Biller Survey, Part Two

The electronic bill payment and presentment industry is entering a new phase of transformation, spearheaded by digital mailboxes and new aggregators.

Boston, September 4, 2012 – A new report from Aite Group examines U.S. billers' current and planned offerings for bill payment channels, payment methods, and bill presentment capabilities, and details the expected transaction growth associated with these offerings. Based on an online March to May 2012 Aite Group survey of 57 U.S. billers, the report also discusses key market issues relevant to Aite Group’s client base: billers' attitudes toward digital mailboxes, card brand and product steering, the value of cards versus ACH versus online banking bill pay, the performance of various bill presentment channels, alternative payments, the state of expedited bill payment acceptance, and vendor brand awareness.

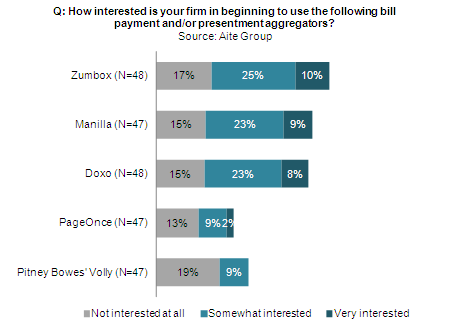

It would be foolish for anyone involved in the bill payment industry—or payments overall—to ignore the changes sweeping the bill payments space. Like other payments areas, the bill payments sector has its startups (BillFloat, Doxo, Zumbox, Manilla), large vendors betting big (Pitney Bowes), new concepts (digital mailboxes), arguments over money (card steering), and a wide host of characters vying for a bigger piece of the bill payments pie. Ubiquitous alternative payment players (such as PayPal) and digital and mobile wallets are also part of the picture.

“The payments industry is undoubtedly facing a period of tremendous change, centered at the moment around the transformation of payments at the point of sale,” says Gwenn Bézard, research director with Aite Group and co-author of this report. “Likewise, the electronic bill payment and presentment industry is entering a new phase of transformation, spearheaded by digital mailboxes and new aggregators."

Companies involved in the bill payment and present industry and referenced in this report are Ace Cash Express, Alacriti, Aliaswire, American Express, Authorize.net, Bill-Me-Later (part of eBay's PayPal), Billeo, BillFloat, BillingTree, BillMatrix (absorbed by Fiserv), BNY Mellon's ClearTran, CDS Global, Chase Paymentech, CheckFree (absorbed by Fiserv), Citigroup, The Clearing House's EBIDS, Discover, Doxo, DST Output, Federal Payments, Fidelity Express, FIS, Fiserv, Fort Knox National, Global Express, Green Dot, Google, Intuit's Mint, ISIS, Jack Henry's iPay, JPMorgan Chase, Kubra, Manilla, MasterCard RPPS, Metavante (absorbed by FIS), MoneyGram, NACHA, NCO, Official Payments (aka Tier Technologies), Online Resources, Oracle, PageOnce, PayDirect, Paymentus, Paymode, PayNearMe, PayPal, Payveris, Pitney Bowes, Precash, QPay, SAP, Softgate Systems, Striata, Tangible, Tier Technologies, Tio Networks, Transactis, TransCentra, TSYS, UDC, Ventanex, Visa, Westen Union, Yodlee, and Zumbox.

This 61-page Impact Report contains 43 figures and one table. Clients of Aite Group’s Retail Banking, Health Insurance, and P&C Insurance services can download the report.