May 2021 – Improving product speed to market depends on optimizing internal processes and technology for life/annuity/benefits insurers. Speed to market is a key concern for L/A/B insurers. Delays in introducing or modifying products can be due to technology issues, product complexity, filing times, or internal business processes.

This study of 38 life/annuity insurers presents data about average speeds to market for new and modified products. It analyzes the factors that correlate to faster speeds for different lines of business.

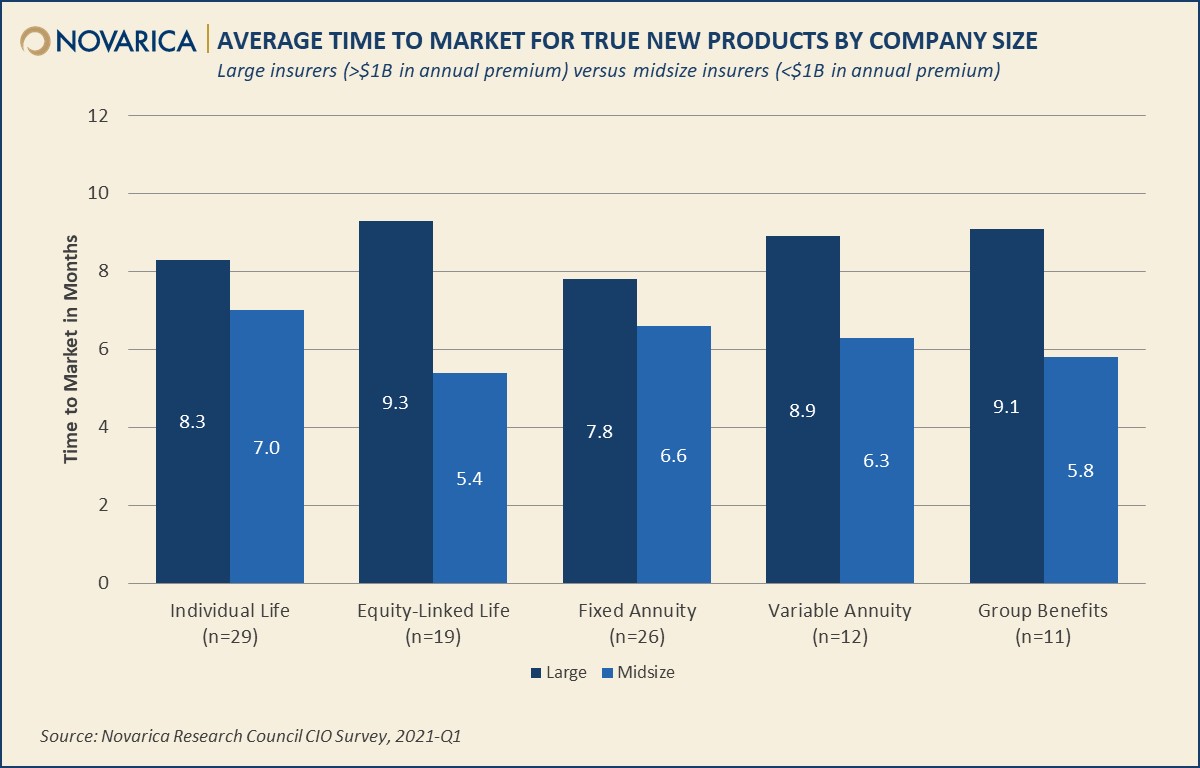

Key Points and Findings

- Smaller insurers are faster. Larger insurers tend to have more complex processes and are an average of 25%-30% slower for new products and modifications.

- Design is the most common long-pole phase for new products, and it can contribute to delays. Insurers whose longest phase was design were a week to two months slower than their peers.

- Newer technology often correlates with faster product speeds. Insurers with more modern core systems (homegrown or vended) tend to have faster product modification times, and larger insurers with modern systems are also faster to market with true new products.

About the Author

Other Authors