Procurement Cards: A Dormant Opportunity

Report Summary

Procurement Cards: A Dormant Opportunity

Though p-cards represent a very small portion of B2B payments, changes in fee structure and card policies could double issuers’ p-card revenues.

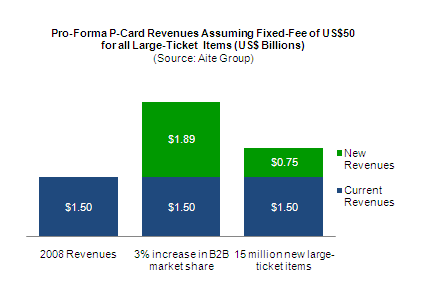

Boston, MA, July 14, 2009 – A new report from Aite Group, LLC compares the primary B2B payment vehicles and discusses the opportunity for growing B2B card revenues. The report evaluates B2B electronic payment vehicles and discusses how procurement cards (aka "p-cards") are best positioned to come out on top, assuming some modifications to the current treatment of B2B cards were adopted. The report makes specific recommendations for card networks, issuing banks, merchant processors and merchant acquirers looking to increase the competitive positioning of the p-card product.  Despite having existed for more than 20 years, procurement cards comprise only a small percentage of the U.S. business-to-business (B2B) payments landscape. Aite Group asserts that p-cards' limited penetration is driven by the structuring of the product rather than a limited market demand. Because p-card transactions are priced as a percentage of the transaction's dollar amount, fixed-fee electronic payment vehicles such as ACH and Fedwire are more competitively positioned for larger-dollar transactions. By taking the actions Aite Group recommends in the report, card networks and issuers can make card payments for higher-ticket items more palatable to suppliers, awakening the dormant p-card opportunity. As a result, Aite Group conservatively forecasts that incremental revenue to card issuers from new supplier acceptance of large-ticket items could reach US$1 billion per year.

Despite having existed for more than 20 years, procurement cards comprise only a small percentage of the U.S. business-to-business (B2B) payments landscape. Aite Group asserts that p-cards' limited penetration is driven by the structuring of the product rather than a limited market demand. Because p-card transactions are priced as a percentage of the transaction's dollar amount, fixed-fee electronic payment vehicles such as ACH and Fedwire are more competitively positioned for larger-dollar transactions. By taking the actions Aite Group recommends in the report, card networks and issuers can make card payments for higher-ticket items more palatable to suppliers, awakening the dormant p-card opportunity. As a result, Aite Group conservatively forecasts that incremental revenue to card issuers from new supplier acceptance of large-ticket items could reach US$1 billion per year.

"This opportunity to expand revenues from p-cards is well within the control of card issuers and card networks," says Judson Murchie, analyst with Aite Group and co-author of this report. "By modifying a few practices and strategies to better position cards for B2B suppliers, p-cards can greatly increase market share."

"Because increased p-card adoption is relative to structural changes," says Nancy Atkinson, senior analyst with Aite Group and co-author of this report, "Aite Group recommends that issuing banks, card networks, merchant processors and merchant acquirers make increasing B2B supplier acceptance a top priority - by changing the high-ticket pricing model, for example - or risk limiting the potential of the product."

This 44-page Impact Report contains 24 figures and one table. Clients of Aite Group's Wholesale Banking service can download the report.