How Banks Can Avoid Disintermediation by Delivering Greater Control of Small-Business Finances

Report Summary

How Banks Can Avoid Disintermediation by Delivering Greater Control of Small-Business Finances

Developing tools for payables, receivables, and cash flow forecasting can improve a bank's relationship with its small-business customers.

Boston, January 31, 2013 – A new report from Aite Group describes three focus areas—payables, receivables, and cash flow forecasting—that are critical for financial institutions striving to better serve small businesses and decrease disintermediation. This report analyzes small-business desires to manage their cash and stretch their dollars and discusses overcoming the challenges of forecasting cash flow, tracking payables, collecting receivables, and processing payroll.

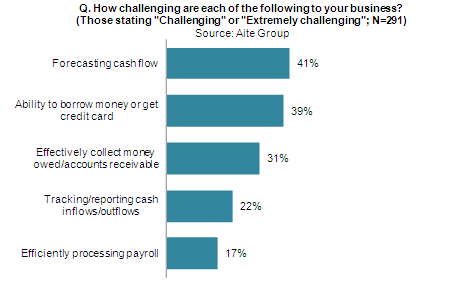

Despite increased bank focus on small-business customers, remaining product gaps are leading to low small-business customer satisfaction and a significant likelihood of customer disintermediation. While this is bad news for financial institutions—particularly for the largest four U.S. banks—it also provides opportunities for banks whose small-business strategies and offerings sing. Among the gaps is cash flow forecasting, a small-business need that banks could meet by integrating bank systems with the processes and systems used to make and collect payments.

“Now is the time for banks to begin addressing their vulnerabilities in the small-business space,” says Christine Barry, research director with Aite Group and author of this report. “They must proactively offer the tools necessary to improve customer satisfaction, address customer inefficiencies and challenges, and increase the utility of their online banking platforms.”

This 18-page Impact Note contains eight figures. Clients of Aite Group’s Wholesale Banking service can download the report.