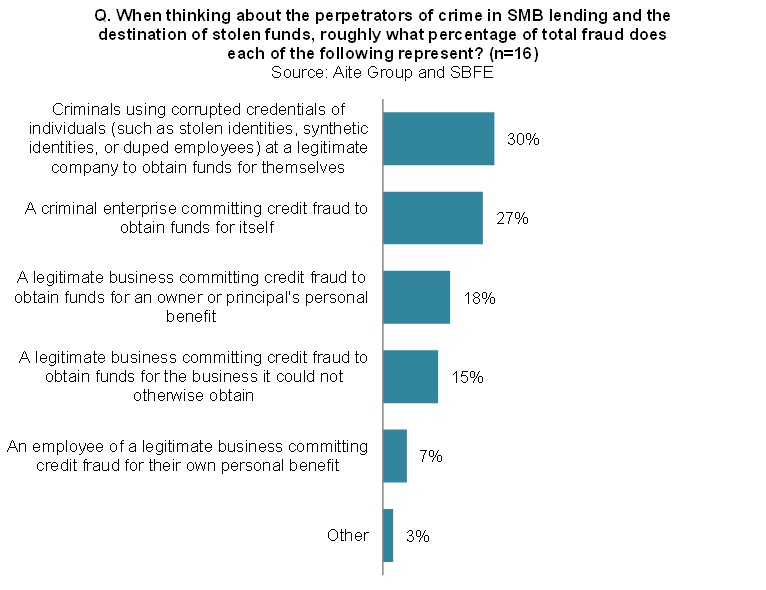

Boston, June 3, 2021 –Vast, wired for speed, and striving for scale, the ecosystems that grant credit to small and midsize businesses are a dream come true for criminals. Wherever transaction speed, rapid capital flows, and pressurized institutions coexist, criminals find exploits—and exploit they do. But financial institutions have begun successfully summoning the technologies and best practices―many originating with the retail operations of their enterprise―required for the successful detection and deterrence of credit fraud.

This annual Impact Report identifies and explores the various fraud vectors in the SMB lending market, their virulence and historical trends, and FIs’ self-assessed levels of preparedness to deter fraud in their SMB lending lines of business. This report is based on a survey conducted by Aite Group and the Small Business Financial Exchange between December 2020 and March 2021 of 32 U.S.-based FIs extending loans to SMBs.

This 33-page Impact Report contains 17 figures and five tables. Clients of Aite Group’s Wholesale Banking & Payments or Fraud & AML services can download this report, the corresponding charts, and the Executive Impact Deck.

This report mentions Accertify, Arkose Labs, Behaviosec, BioCatch, Bolt, buguroo, Callsign, Cleafy, Daon, DataVisor, Decision Logic, Dun & Bradstreet, Entersekt, Entrust, Equifax, Experian, FICO, FraudHunt, IBM Trusteer, ID R&D, IDMERIT, Incognia, IPQualityScore, Kofax, LexisNexis Risk Solutions, MaxMind, Nethone, Neuro-ID, Neustar, NuData Security, OneSpan, Oneytrust, Optimal IdM, Precognitive, Ravelock, RSA Security, Samsung SDS, SBFE, SecuredTouch, SEON, ThreatMark, TransUnion, TypingDNA, and XTN Cognitive Security.

About the Author