The Case for Direct Deposit Advance

Report Summary

The Case for Direct Deposit Advance

U.S. financial institutions could generate US$500 million in revenue by marketing direct deposit advance to customers who currently use payday loa

Boston, February 1, 2012 – A new report from Aite Group presents a business case for banks and credit unions to generate revenue through direct deposit advance. Based on a February and March 2011 Aite Group survey of 500 U.S. consumers, the report sizes the potential market for direct deposit advance and provides demographic information on payday loan borrowers.

Though controversial, payday loans are viewed by the underbanked and unbanked as preferable to paying banks’ non-sufficient funds (NSF) fees—fees placed on bounced checks and overdrawn debit cards. Rightly so: Aite Group research has shown that payday lending is significantly cheaper than NSF if the product is truly used for short-term financing. There is, however, a competing product that just a handful of banks offer today: direct deposit advance. Conceptually similar to payday loans, direct deposit advance differs from payday loans because it 1) is offered only to existing bank customers who deposit their paycheck directly into the bank; 2) has lower interest rates than traditional payday loans; and 3) in most cases limits the amount a customer can borrow to a maximum of US$500.

“Banks and credit unions have a significant opportunity to generate revenue by marketing direct deposit advance to customers and members who currently use payday loans,” says Ron Shevlin, senior analyst with Aite Group and co-author of this report. “By cannibalizing online payday loans, direct deposit advance could generate US$500 million in revenue for U.S. banks.”

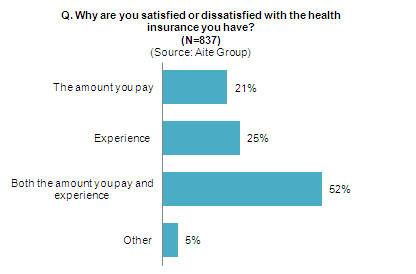

This 17-page Impact Note contains nine figures and seven tables. Clients of Aite Group’s Retail Banking service can download the report.